🎉 Tillful is now part of Nav! Find the best small business loan at Nav

Hey Tillfulers,

In light of Divvy closing its credit builder program, I wanted to take a moment to reaffirm that Tillful is committed to serving small business owners.

The past year has been hard for SMB’s. PPP is a thing of the past, and most of the COVID tax credits ended in 2022. With interest rates rising, many fintech providers have been shutting down their SMB services. We’ve seen Brex drop their small business products, Wells Fargo close their secured business credit card, AtoB tighten up their requirements, and now, Divvy closing their credit builder program.

As a team of finance professionals, we get as much as the next guy that the smallest, newest businesses are seen as risky bets. The difference for us is that we believe these businesses are not as risky as they may seem by the surface-level numbers, and we’re all-in on proving that, providing the tools to help them become credit visible. It’s all in our founding mission — unlock credit and capital for credit-invisible and underserved businesses. In fact, we’ve strategically taken resources away from our enterprise solution, and applied them to Tillful, because we believe in this so strongly. We have skin in the game — this is not an experiment for us.

Serving small businesses has always been our focus. It’s not a surprise to us that financial providers have now pulled out of SMB’s. We’ve witnessed this as recently as during 2020 — in roughly March through September, lenders stopped providing funding due to uncertainty. Remember that brief market crash? Small businesses tend to get the short end of the stick in times of crisis.

As for fintech lending, post-stimulus markets were good and rates were low, so VC money was flowing. It was a good time to expand, giving generous perks along the way. Now, the fintechs that were winning by losing money to gain market share are no longer able to do that. So, they left. The cycle repeats.

Tillful has engaged in responsible growth since day one. Our core focus was to help SMB’s build credit, and not simply to buy growth. We made sure that all of our numbers were sustainable, because we saw this coming, and we wanted to be there for you even when markets went south.

I share all this with you because I know that there is some fear and uncertainty around what has been happening, and we want to be as transparent as we can with you. Tech is tightening up, and your business credit and funding options are going to be more limited. We’re certainly not immune to the economic headwinds, but we’re standing our ground in the face of them.

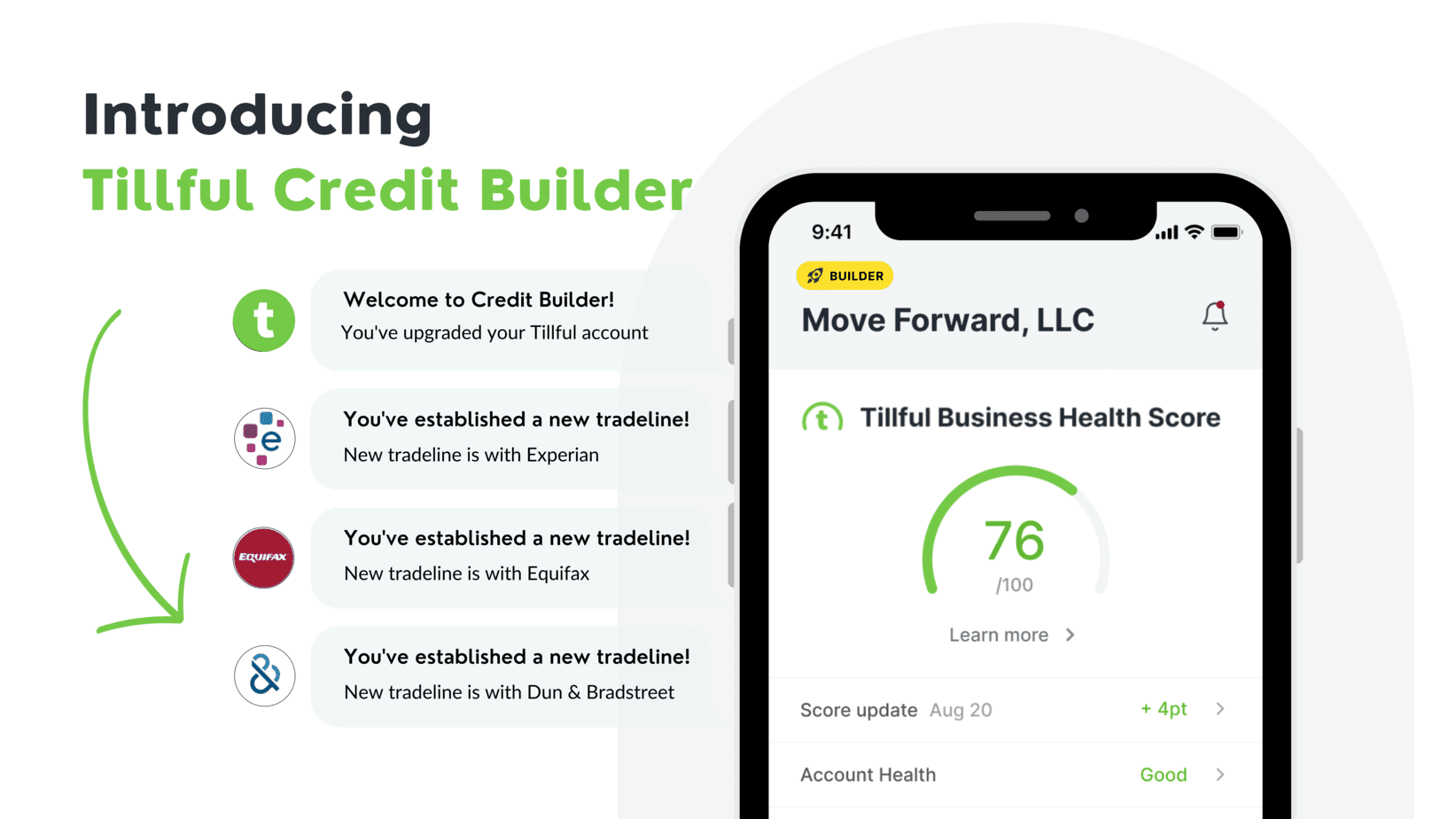

Tillful Card is one of the last credit builder cards available for small businesses. We report to all three credit bureaus (Experian, Equifax, and Dun & Bradstreet when you self-report). We’re very thankful for your support thus far, and we look forward to partnering with you to unlock the credit your business deserves.